I’m reading Your Money or Your Life, a classic on Financial Independence. It’s filled with tactics and tools, some practical, some debatable, but this isn’t a summary. What fascinates me about the book are a few key ideas that make you rethink the relationship between money, time, energy, and happiness.

How Much of Your Life Are You Spending?

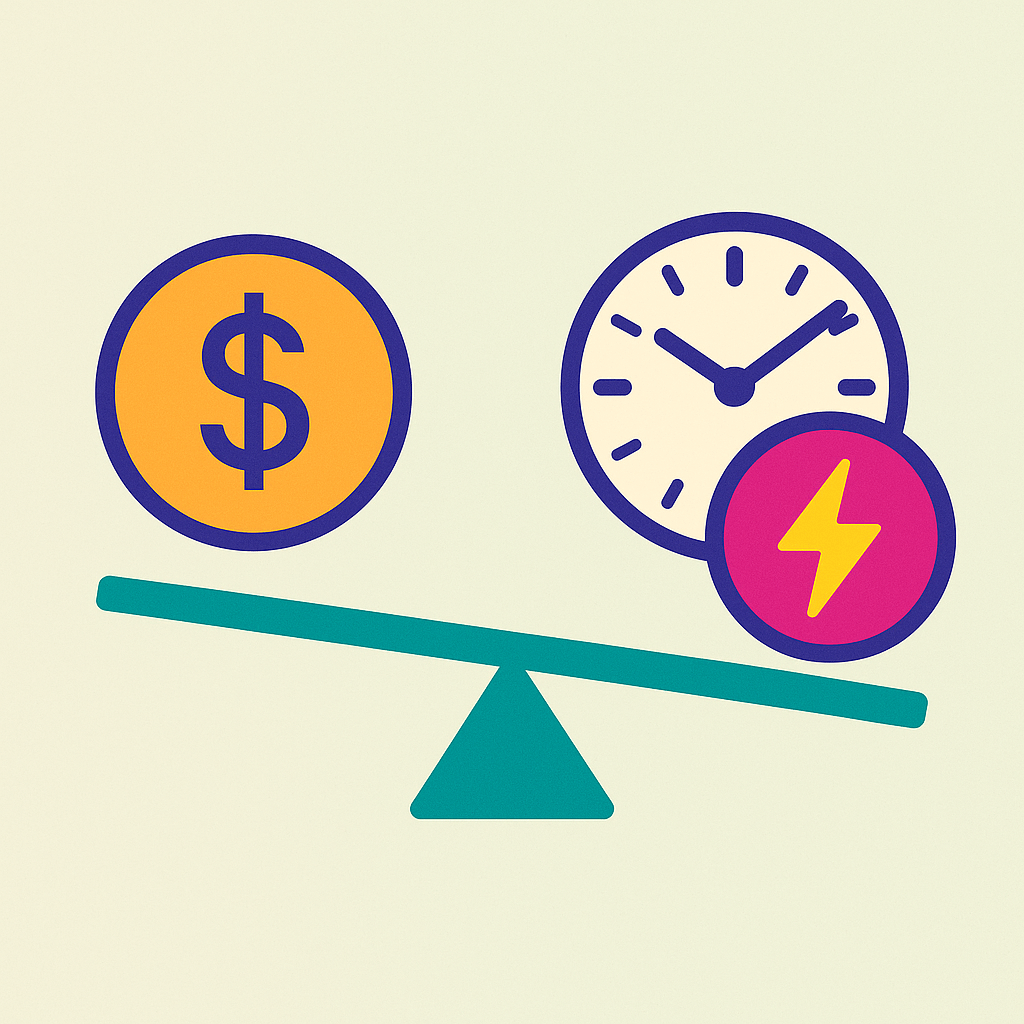

The most powerful lesson in the book is to measure every expenditure as an exchange of time and energy.

Instead of asking, “Can I afford this?”, ask, “How many hours of my life will this cost me?” Calculate your real hourly wage after taxes and expenses, and use that to measure every purchase. Suddenly, each expense becomes tangible. Those shoes don’t cost $150, they cost six hours of your freedom.

This perspective transforms spending from a blur of digital transactions into something real. You start to see that every swipe of your card is a small trade of your life energy.

Even the way we pay changes how we perceive spending. Paying with cash is psychologically the most painful. You literally hand over your money and feel it leave your pocket. Debit cards are easier; you only see the loss later when you check your bank statement. But credit cards are the most dangerous—they create an illusion of affordability. You don’t feel the loss until the bill arrives, usually when it’s too late.

Thinking in terms of time and energy works better than any budgeting app and takes the payment method illusion out of the equation. It connects money back to its source: your life.

The Cost of Boredom

The book also touches on a subtler truth, one I’ve often seen in myself. Free time isn’t always free.

When we’re bored, we start spending. “Maybe I’ll buy a better coffee machine.” “Maybe a new lens will make me take better photos.” Boredom leads to consumption because it makes you think that a purchase can fill the void.

But what we really crave in those moments isn’t an object, it’s meaning, stimulation, engagement. Dopamine is the chemical disguise of emptiness.

The solution isn’t to stop spending altogether. Spend on your interests, not your impulses. Use your resources to feed your creativity, not your cravings. If photography makes you feel alive, buy the gear you’ll actually use. But make sure it’s the act of creating that fulfills you, not the comfort of owning things.

Don’t become the person who owns the best camera, lens, and gimbal, but never takes photos.

How We’re Trained to Consume

Spending money when bored is not your fault. Impulse buying isn’t a flaw of character; it’s a product of design. Modern marketing is engineered to make us feel incomplete.

We’re sold the idea that consumption is self-improvement. “Invest in a new keyboard to boost productivity.” It’s all the same illusion, objects dressed as progress and investments.

Even our leisure has been monetized. We’re told where to drink coffee, where to be seen, what to wear, and how to signal belonging. The fashion industry is the perfect example: clothes that are perfectly functional become “obsolete” overnight. And the cruelest part? Many buy the yoga pants without ever doing yoga.

When people spend money for approval, marketers win, because the hunger for validation never ends. You can always have more stuff, you can always be richer.

“Men do not desire to be rich, only to be richer than other men.”

John Stuart Mill

From Riches to Fulfillment

Being “rich” is comparative, it’s always in relation to someone else. Fulfillment, on the other hand, is personal. It can’t be measured, copied, or competed over.

Fulfillment takes you off the racetrack. It declutters your life and redirects your energy toward what truly matters: family, hobbies, learning, small luxuries that align with your values.

To me, mindful spending isn’t about restriction, it’s about alignment. I use one simple test for larger purchases: frequency of use.

If I buy a new coffee grinder, I don’t see it as a luxury. I use it every day, and I deeply enjoy making coffee. That’s worth it. But my camera, which I use only on trips, doesn’t need a new lens or body. It already serves its purpose. If I ever want to become a better photographer, I can invest in a course and buy better gear when I become a better photographer that spends a lot of time taking photos.

Spend more where you live more. Spend less where you merely escape.

The goal isn’t to own less—it’s to own consciously. Every dollar you spend is a choice about how to use your life energy. Make it count.